Shipping goods across the globe should feel like a well-oiled machine when you’re partnered with a trusted freight forwarder. But even the most carefully planned shipments can be derailed by unforeseen events like natural disasters, theft, or equipment failures. For cargo owners without insurance, these disruptions can lead to significant financial losses, threatening their operations.

That’s where Shipper’s Interest Insurance comes in. In this guide, we’ll explain the basics of Shipper’s Interest Insurance, why it’s crucial for your shipping strategy, and how OpenRoad can help you protect your assets with ease.

What Is Shipper’s Interest Insurance?

Shipper’s Interest Insurance is a safeguard for cargo owners, offering financial protection against damage, theft, or loss of goods in transit. It covers shipments moved by truck, air, ocean, or rail and shields against risks such as:

- Physical damage

- Total loss of goods

- Natural disasters

- Theft or piracy

- Accidents or mechanical failures

With Shipper’s Interest Insurance, cargo owners can confidently navigate the complexities of global trade, knowing their valuable goods are secure.

Fun Fact: The ancient Babylonian ‘Code of Hammurabi’ created in 1754 BCE outlined a system where a person receiving a loan to fund a shipment of goods would pay the lender an additional fee in exchange for the lender’s promise to cancel the load if the shipment was stolen — modern-day shipper’s interest insurance!

Why Is Shipper’s Interest Insurance Important?

Many cargo owners mistakenly assume that carriers or freight forwarders are responsible for any damage or loss during transit. However, most carriers have limited liability and may not cover losses caused by factors beyond their control. This leaves cargo owners exposed to potentially devastating financial risks.

Common risks in global shipping:

- Earthquakes

- Severe weather

- Piracy

- Jettisoned cargo

- Faulty equipment

- Terrorism and war

Shipper’s Interest Insurance minimizes financial exposure, ensuring that your business can recover quickly from unexpected events.

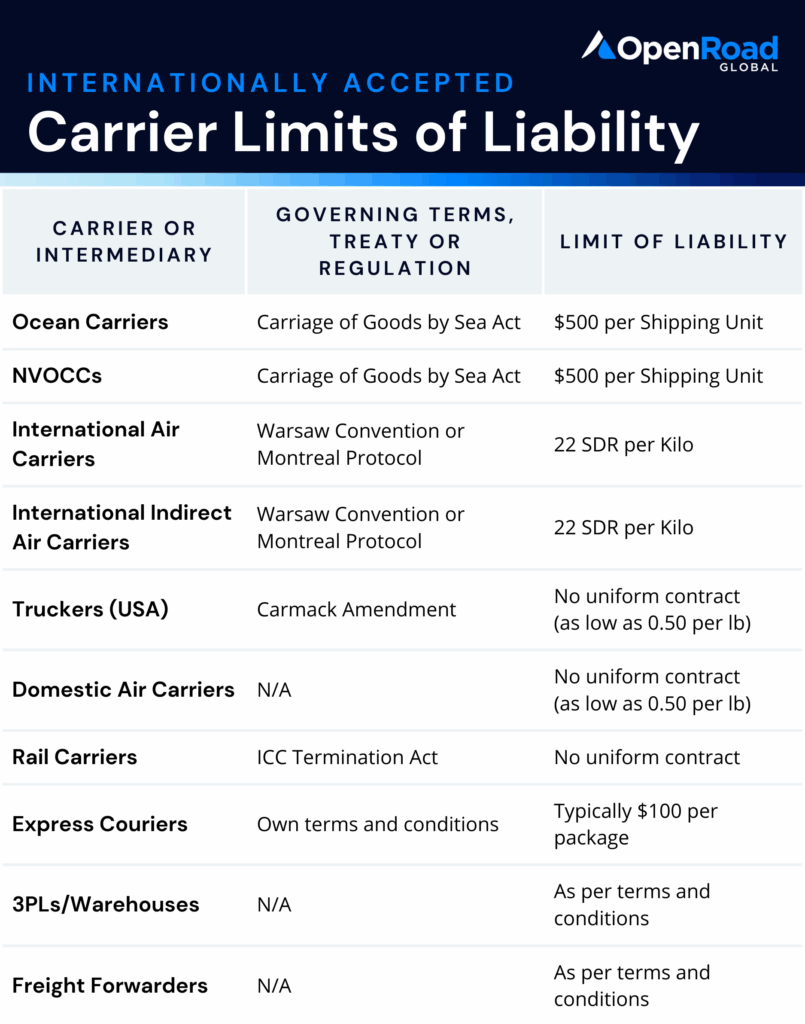

Understanding Your Liability: Mode-Based Exposure

Liability in the event of loss or damage varies depending on the mode of transport. There are internationally accepted standards that outline these limits of liability:

Understanding these limits is key to assessing your exposure and ensuring proper coverage.

General Average: A Maritime-Specific Consideration

One unique principle in ocean shipping is General Average, which distributes losses from sacrifices (e.g., jettisoning cargo) or expenses (e.g., towing) incurred during a sea voyage across all stakeholders, including other cargo owners and sea vessel owners. It is based on the idea that the cargo and the ship are interdependent and that all parties should share in the costs of losses incurred to save the ship and its cargo from peril.

For example, if a ship jettisons cargo to prevent sinking, the remaining cargo owners must contribute to the losses. A cargo owner’s financial responsibility is proportional to their cargo’s value.

Key takeaway: Cargo affected by General Average won’t be released until a financial guarantee is provided. While General Average declarations are rare, understanding this principle is essential when shipping by sea. Having appropriate insurance coverage in place will mitigate the financial risks associated with a general average declaration.

How to Analyze Your Risk

Assessing your risk helps determine the level of coverage you need:

- What are the Terms of Sale? Clarify with trading partners who is responsible for insurance. Even when the Incoterms specify the responsible party, it’s a good idea to communicate with your client/vendor so there are no misunderstandings.

- What is the Mode of Transport? Each mode has unique liability limits, as mentioned above, so evaluate your shipment accordingly.

- Are there Extreme Risks? Identify factors like piracy-prone routes, seasonal weather hazards, and high-value cargo visibility.

Proactively analyzing these risks ensures you choose the right protection for your cargo.

How to Get Shipper’s Interest Insurance

When it comes to securing coverage, cargo owners have several options:

- Self-Insure: For those with substantial resources and a high risk tolerance.

- Through a Freight Forwarder (Recommended): Convenient and efficient, with experts handling paperwork and claims.

- Purchase Your Own Policy: Offers control but requires time and investment.

- Declare Value to the Carrier: Limited liability coverage, often with higher premiums.

Why Choose OpenRoad for Shipper’s Interest Insurance?

At OpenRoad, we advise our customers to obtain insurance, and we offer robust coverage should they choose to use our insurance services. Here’s why shippers trust OpenRoad for shipper’s interest insurance:

- No upfront deposits: Enjoy flexible, pay-as-you-go options.

- Reduced administrative burden: We manage the paperwork for you.

- Tailored coverage: Our experts help you navigate your unique needs and risks.

- Expert claims handling: In case of loss, we facilitate the entire claims process.

Protect Your Assets Today

Shipper’s Interest Insurance is a smart investment, providing essential protection against shipping uncertainties. By taking proactive steps to analyze risks and secure the right coverage, you safeguard your business and ensure a seamless supply chain.